How Great Companies Get Disrupted

The nature and pace of change in the modern economy pose an existential threat for most established companies. They often faces challenges rooted in a combination of mindset, skill sets, organization, and process; the same capabilities that enable companies to thrive often constrain them when it comes to quickly adapting to a changing market.

It was 2016, and a Fortune 500 CIO sat in our offices describing how market changes were threatening the continued existence of his entire company.

“For us, innovation projects mean five years, fifteen million dollars, and nothing to show for it,” he lamented.

How is it that even in the face of existential threats many organizations are unable to effect significant change?

It’s not because they’re not capable people. It’s rooted in their attempt to apply their existing organizational structures and strategy to endeavors that require a very different approach. The solution is intuitive—once it’s explained.

In a previous article, we explored some of the ways disruption is fundamentally different from optimization:

- V.U.C.A (Volatility, Uncertainty, Complexity, and Ambiguity)

- Changing hearts, minds, and behaviors

- Much higher risks

- Higher volatility

- Complexity and coordination challenges

- Faster cycles

- A much longer arc

These are the reasons why traditional management best practices to break down in the context of disruption.

Traditional organizations struggle to keep up with the market

Traditional management orthodoxy is based on the concept of building an organization optimized for your business model, resources, context, and other factors. Once you’ve honed in on that model, your goal is to stay ahead of the competition through a combination of effective execution and incremental innovation to maintain your competitive edge.

The problem is that’s not good enough any more. Market changes are increasingly disruptive. And they’re starting to happen so quickly that by the time your organization adapts, the market has already moved on. It’s expanding a highway highway but by the time the work is done the traffic has already exceeded the new capacity.

“Any plan conceived in moderation must fail when the circumstances are set in extremes.”

— Klemens von Metternich

Mindset

Existing companies all started—at some point—with a very small team. There may be exceptions to this, but by-and-large, it’s true. As teams grow, they form into a mature organization and naturally build a mindset and a set of processes suited to the execution of their business model. If not, they can’t survive. Unfortunately, the same things that enable a big company to operate at scale become what makes it so hard for them to adapt and change.

Mindset is the collective worldview, identity, and knowledge of the organization. It forms based on what works over time, and becomes established as a set of norms, expectations, and understandings. “Our customers value a personal relationship with us” and “our customers care about price but will only accept minimal unreliability” are two simple examples.

An organization’s mindset is unique and powerful, serving a critical role in enabling effective collaboration and goal-setting. But mindsets tend to calcify over time. What works in the beginning may not work in a rapidly changing world, and certainly tends to break down when it comes to breakthrough innovation.

“We don’t see things as they are, we see them as we are.”

— Anaïs Nin

Head In Sand Disease

Unfortunately, true beliefs often end up persisting past the point of truth. Here are just a few examples of famous examples of what we call HIDS—Head In Sand Disease.

“Television won’t be able to hold onto any market it captures after the first six months. People will soon get tired of staring at a plywood box every night.”

— Daryl Zanuck, Co-Founder of 20th Century Fox

“I think there is a world market for maybe five computers.”

— Thomas Watson, President of IBM in 1943

“There is no reason anyone would want a computer in their home.”

— Ken Olsen, founder of Digital Equipment Corporation, 1977.

“Google’s not a real company. It’s a house of cards.”

These attitudes illustrate a much more pervasive and troublesome reality: most people in an established organization suffer from myopia about their own industry when it’s undergoing disruption, or when it’s ripe for it. All too often they fail to see or accept meaningful changes occurring around them and to capitalize on huge opportunities for change. This limits their ability to adapt. And the problem is most acute in the context of the type of significant changes that occur in the context of disruption.

Looking at the future through a keyhole

Even when significant change becomes unavoidable, organizational mindset tends to limit the ability of even the smartest people to determine the best path forward.

“People working on a particular set of issues use frameworks that are optimized for addressing the questions of that domain…”

— Greg Satell

Sometimes you know so much about a domain, and have so much expertise in solving problems within it, that you struggle to understand or adapt to the new frameworks required for where your industry is heading. Here’s an example from The Verge about how Microsoft missed the boat on mobile:

“Instead of focusing its engineering efforts on Windows Mobile, Microsoft was too invested in desktop PCs and its success at dominating that category of computing. Windows Mobile … [was] designed to look like a miniature version of Windows right down to the Start menu. Microsoft was obsessed with having Windows everywhere. Apple introduced a smart and simplistic mobile alternative to Windows, and the industry followed its path — Microsoft included.”

This manifests itself most commonly as an inability to perceive the best opportunities for adaptation and a failure to execute efficiently when pursuing the opportunities that appear most promising.

Brand & identity

Organizations have an identity, complete with values, aspirations, and other human traits. It’s formed by the collection of people involved—and also exists at a combinatorial level that transcends the sum of the parts. That identity might not be clear or consistent. And it might not be appealing. But it’s there. And it’s powerful.

The public manifestation of identity is your brand. Brand identity can be a powerful tool for establishing credibility and trust in new product introductions and for weathering storms of controversy.

But identity can also be a limiting factor, both internally and externally. As we discuss elsewhere, it’s very important for your customers, team, and partners to have a stable understanding of who you are and what you stand for. Trying to adjust that in any meaningful way either may not be credible, or may be met with distaste.

Take, for example, Colgate’s attempt to introduce frozen meals in the 1980s. Toothpaste and food—yummy! You can imagine the commercial reception it received.

When established organizations with strong identities attempt to adapt to new markets, it can be quite difficult to maintain continuity and credibility with customers, team, and partners. In some situations that alone can be sufficient to doom a disruption effort.

Skill sets

Disruptive innovation requires frontier expertise and an entrepreneurial mindset. And the specific domains involved are likely to evolve very quickly—often more quickly than an enterprise is equipped to respond.

Every large organization has at least some of the talent it needs for disruption. Many have a lot of it. Unfortunately, that talent is typically in extraordinary demand in the context of the core business, and ends up being disallowed from disrupting.

“To actually get something going in a large organization, you need the ideas and you need the people who believe in them, but the people who are actually capable of these things are the good ones, and they are already stretched by their work in the corporate environment…. It [becomes] impossible for them to pull it off.”

— A New Model For Innovation In Big Companies, HBR

It’s also very difficult to attract the most desirable disruption talent, which is increasingly drawn to either the big tech companies or exciting startups. And when an enterprise is able to successfully recruit that sort of talent, it’s often hard to retain and cultivate it.

The problem of promoting from within

Promoting from within tends to lead to homogenization over time, and the development of personal power bases. That tends to conspire to create a reinforced mindset and reduce agility and adaptability. It also tends to constrain idea generation and creativity Even when promotion from within isn’t occurring, human tendencies to hire like people can easily lead to a similar outcome of bringing on like-minded people.

Disruption requires creativity, idea generation, and exploration of the frontier. Reinforced mindsets and homogeneity tend to nip disruption in the bud.

Organization

Organizational design is another area that often constrains enterprises seeking to disrupt. It occurs naturally (and often consciously) over time in the face of challenges maintaining order, stability, and accountability in larger organizations.

Organizations naturally grow to adapt to the market in which they form, and optimize over time to execute their business model with maximal efficiency. That often takes the form of increased hierarchy and division of labor. Those organizational paradigms are useful for preserving unambiguous accountability and risk reduction (e.g., finance, HR, legal, IT, and procurement).

“[Hierarchy] is the only form of organization that can enable a company to employ large numbers of people and yet preserve unambiguous accountability for the work they do.”

– Elliott Jaques, “In Praise of Hierarchy” HBR 1990

Division of labor is often employed to optimize operations in large or complex systems. This is especially important as the stakes of failure increase. Legal, procurement, IT, financial controls, and other duties become increasingly important with scale. Each duty also becomes increasingly complex as it concerns a larger and more complex parent system. This leads to further abstraction of complexity in the form of sub-group hierarchy and divisions of labor.

But they quickly break down when adaptability and risk tolerance become important, such as in the context of disruption. The new economy (with its faster cycles) has made those more traditional organizational forms broadly less desirable.

The Gilded Age of enterprises of the mid 1950s saw the rise of extraordinary organizations with massive scale and far flung assets. But disruptive new technologies toppled even the kings of the hill. Organizational design played a key role in their demise.

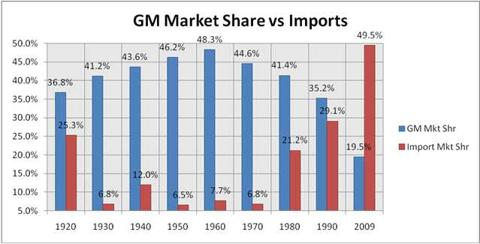

A car for every purse and purpose

Alfred Sloan’s vision for GM was a company that would serve “every purse and purpose,” which led to a proliferation of product offerings and brands to serve as many customer segments as possible. GM built an extraordinarily successful company around its ability to direct and coordinate a far-flung set of internal and external (supplier) value creation units. By 1953, General Motors employed one out of every 200 working people in America and accounted for 3% of the country’s gross domestic product.

But as new design and manufacturing models emerged—for example the Toyota Production System and the evolution of lean manufacturing—that resulted in shorter cycles and superior product qualities, GM began to struggle to adapt its existing organization to a new way of doing things. Top down decision-making was fundamentally misaligned with these new approaches that enabled new competitive advantage through shorter cycle times and closer adherence to customer needs.

The problem was that General Motors was designed and optimized for the prior economy, and was unsuited—effectively by design—for the new economy brought on by technological change.

Everyday low prices

Walmart built an extraordinary organization in the late 20th century that functioned so well that it seemed unstoppable. Their entire system was built around delivering the best prices everyday to everyday people.

From “What is Amazon” by Zack Kanter:

"Walmart managed against a hard constraint: the shelf space available in a 200,000 to 300,000 square foot retail store near where their customers lived. They realized that stocking store shelves was a zero sum game, and they optimized their entire business around this. And it worked spectacularly well.

Until Amazon showed up. Jeff Bezos realized that the world was entering a time of infinite shelf space. Freed of that constraint by new technology, he designed an organization that optimized for the broadest selection, fast and reliable delivery, and easy returns. Walmart’s future was written in 1994, although they didn’t know it. Perhaps they can continue to muscle against Amazon over the coming years, but the reality is that they’ll never be the same as they once were."

In many cases the very superpowers that emerge during the formation of a successful organization are the same reasons they fail to disrupt thereafter.

Risk mitigation misalignment

When the CRM goes down, IT is typically castigated but sales is rewarded when it works. The same applies to procurement, legal, HR, IT, and other groups that almost inevitably (and often by design) function as risk mitigators rather than value creators.

This might work in the context of a stable organization where rationally planned initiatives can push their way through the risk mitigation organization without too much damage or time passed.

But it’s almost certainly a death sentence for most disruptive innovations, which present as highly risky to these organizational elements and thus typically end up dying or being watered down to the point of obscuring the original intent.

Organizational debt

Big companies have lots of hard assets, but those assets aren’t as valuable as they used to be. As markets change ever more quickly, having certain assets can become a liability. Essentially, just as an organizational design can be suited to one market era, but poorly designed for another, so can it be for assets.

Hard asset debt

Take, for example, a far flung logistics system. Built over the course of years and tremendous capital expenditures, it may provide significant competitive advantage in one era. But in a new era, those same assets may turn into a loadstone, perhaps as the market evolves towards a 3PL model as margins are squeezed and customers demand fine control and individualized solutions.

Technical debt

Another organizational debt that many enterprises fail to take into account is technical debt. The same technology infrastructure that in one era provided significant advantages may become an impediment in later eras. Take for example, the country of India, which has long had a mobile infrastructure far better than that of the US. It occurred because (under the guidance of my friend Sam Pitroda) India skipped the landline telephone era, and instead allocated capital and infrastructure to a new, more advanced, technology paradigm.

It’s easy to assume that technology development flows from version to version, with each building upon the last. The reality is far more treacherous. In fact, technology often requires rebuilding (in part or in full) prior technology infrastructures. In those cases, maintaining and working with the prior technology stacks represents a significant impediment to forward motion and flexibility.

Internal sales friction

Executives at large organizations tend to be very aware of the difficulties inherent in pushing disruptive initiatives through internal risk management and resource allocation systems. That makes executives reluctant to undertake risky endeavors; even if they’re willing to risk their reputations on an initiative, they have to consider the sheer level of effort and political capital required to make them happen.

Furthermore, when executives have committed to a disruption initiative, it’s hard for them to admit defeat given all the trouble they have gone through—and the political capital they’ve deployed.

As a result, enterprise disruption initiatives often end up being throttled or killed before they’re even started. And the few that do start are likely to draw time and money even if they’re not performing well.

Corporate politics

The most fundamental reason for the development of internal politics derives from distributed organizational structures and disparate reward systems. Take, for example, the IT department which as we mentioned is castigated when the CRM goes down, while the sales team get all the credit when sales beats targets. The IT team’s natural response is to block any changes that might threaten the stability of technology systems.

These structural conflicts of interest result in subtle, but powerful, forces against innovation. That tends to kill initiatives before they even start, and puts stress on the ones that do somehow launch.

Sometimes the forces aren’t particularly subtle. Take for example, Microsoft’s ill-fated Kin phone as described in an Engadget article:

“While it's hard to argue that Kin is an awful product, the saddest part of the story is that many of the people responsible for it knew it was—they were largely victims of political circumstance, forced to release a phone that was practically raw in the middle.”

It’s a story of corporate politics and how power plays can so easily doom even the most critical disruption efforts.

Coordination challenges

The larger an organization, the harder it generally is to explain new initiatives sufficiently well to organize, energize, and coordinate the (often far-flung) teams required to implement innovation initiatives.

“At a certain point, the gains from economies of scale are defeated by the costs of bureaucracy.”

– Steve Denning, explaining Ronald Coase’s “Nature of a Firm”

There are only so many initiatives that can reasonably be pushed through an existing organization at any given time. This also means that frequent changes can feel like whiplash, followed by the onset of fatigue and confusion. As a result, larger organizations tend to be cautious about introducing too many innovations at a time, or in fact, over time.

Unfortunately, this exists in direct conflict with the need for a portfolio of disruption efforts to manage the volatility inherent in such efforts.

Process

Successful organizations establish processes designed to support the execution of their business model at scale. They’re optimized for efficiency, reliability, and predictability. While critical for surviving in a competitive market, that’s often poorly suited to a disruptive one, which requires innovative idea generation and multiple concurrent experiments, and involves significant volatility and a high rate of failure.

Risk management

When you’re trying to protect a multi-billion dollar business from, for example, a data breach, it’s natural to implement rather draconian procedures to minimize the risks of a breach. Most companies end up with a long list of checklists and approvals required for any new initiative. That friction greatly reduces the number of initiatives that can realistically launch in any given time period. And most initiatives are killed before they can even launch.

“While entrepreneurs are generally accountable to only a small group, intrapreneurs are not afforded that luxury. They must carry out their work within the large, often complicated, infrastructure of a parent company.”

— Gabe Vehovsky in Kellogg Insight

From a procedural standpoint, this typically manifests as approval requirements (otherwise known as death warrants) for anything that touches key risk areas such as IT, regulatory, or the like.

Disruption presses enterprise risk hot buttons almost by definition. Disruption is almost always a messy business involving uncertainty, risk, and volatility. In its natural state, a large enterprise will kill disruption almost every time before it even starts. And when “disruption” does actually survive the gatekeepers, it’s almost always watered down to the point of uselessness.

Missing sense of urgency

At their core, organizational processes tend to focus on avoiding loss over achieving gain. That’s in part driven by the relatively narrow band of upside potential for any given corporate initiative relative to the substantial risk of harming the core.

But the new economy is different. The core is at risk anyway, and the risk only appears to be deepening. Disruption is also different in that successful disruptions have extremely high theoretical upsides relative to their capital requirements. In other words, you might make billions, but you’re unlikely to lose billions trying.

That enterprise focus on loss avoidance, combined with the challenges inherent in predicting disruption upside, means that enterprise capital (both money and influence) allocations often fail to adequately consider the ROI potential for disruption. “You might make a lot of money, but it sure seems risky.”

And yet, one of the key attributes of a successful disruption organization is that it cares more about missing opportunity than failing along the way. The same processes that ensure largely efficient resource allocations in the context of doing normal business are ill suited to disruption projects.

Maladapted resource allocation models

We discussed flawed risk assessment above. Maladapted resource allocation models are a related problem. Even when the will exists to pursue disruption, and teams are able to sidestep risk mitigation death traps, resource allocation processes typically fall down on the job.

What goes wrong?

Established organizations, particularly large ones, tend to make key strategic errors in their approach to allocating resources to innovation:

- They allocate resources inefficiently, often manifested as overallocation in any given initiative

- They pursue too few initiatives at a time relative to volatility

- Approval processes steer budget away from disruption efforts

- They fail to kill initiatives that are obviously not working

Budgetary timeframes

Resource allocation models at large organizations naturally evolve to accommodate evolutionary change, but tend to break down for more innovative projects. Project budgets tend to be at least annual, and often exist in the context of multi-year arcs. Finance teams employ repeatable tests for ROI (e.g., hurdle rates) to ensure capital is being allocated efficiently.

But real innovation involves significant uncertainty—after all, by definition you’re doing something new. In most cases you have few proxies or benchmarks to apply. It’s extremely difficult to predict how much money you’ll need, and when. All of that makes it hard to comply with standard financial approval processes.

So instead of trying a lot of small things, it becomes easier to go to finance with an ask for a substantial capital allocation based on forceful assertions about how successful an innovation initiative is likely to be. That naturally throttles the number of initiatives explored, and tends to filter out the riskier initiatives for which it’s harder to prove an ROI. It’s also a root cause for the frequent over-allocation that occurs, as well as the extended denial when things aren’t working out.

Comfortable with big swings

Unfortunately for enterprises, the market can always afford to fund more and broader experiments than any one enterprise. That puts enterprises at a fundamental disadvantage in terms of portfolio math right from the start. To make matters worse, most enterprises struggle with pursuing anywhere near the volume of disruption opportunities they need to manage the inherent volatility.

One very common reason is that established organizations tend to lump everything into one or two big swings since it’s what they’re most comfortable with. They’re used to succeeding—for the most part—with all of their major initiatives. Given their usually good track record, they tend to think of idea generation and exploration as “one and done” and usually in the context of strategy initiatives. So when enterprises do take risks, they tend to be calculated and concentrated. After all, it’s much more efficient to put your muscle behind a few key initiatives than to focus on lots of small ones.

Imagine going to your boss at GM with ideas for ten new types of jet engines, each more innovative than the next. She’s going to sit you down and tell you to focus—if she doesn’t throw you out of the building first.

But that’s not how things work in disruption. Disruption is an ongoing activity that requires a sustained underlying capability and process. In most cases you don’t even know if it’s going to work out until significant time has passed.

Managing to short term outcomes

While established organizations prefer to budget over longer timeframes, they tend to manage to quarterly outcomes. That’s particularly common in public companies. It’s very rare for established companies to manage effectively across both short and long term horizons. Because disruption tends to take time, most companies end up shouldering it aside in favor of “making the quarter.” When it comes down to a question of allocating time and resources to hitting targets vs disruption, targets almost always win out.

Terrible at pulling the plug

One of the most important parts of disruptive innovation is the art of knowing when to pull the plug on a disruption effort. Many will fail despite how promising they originally appeared.

Enterprises are typically unskilled at identifying what’s not working in the context of disruption, and they tend to be even worse at terminating the ones they know aren’t doing well. In many cases, influential players in the organization are involved in the effort, capital has been allocated, and predictions have been presented. Just as there was little perceived organizational capital to be gained from approving a disruption initiative, there may be even less perceived capital for killing one.

That’s a drag on capital, attention, and long-term credibility. And it’s one more reason why established organizations tend to fail at disruption.

Paradox of Plenty - and of scarcity

The Paradox of Plenty is an economic concept that attempts to explain how and why the countries with the most valuable natural resources tend to be the countries with the weakest economies. It’s rooted in the fact that when people are living in a time of plenty, they tend not to plan ahead adequately for the future, resulting in underinvestment.

We see the same sort of dynamic playing out at many enterprises. When things are going well, enterprises defer longer term investments in favor of investing in the Golden Goose that’s laying the eggs. In essence, they allocate to sustaining activities over disrupting ones.

Perversely, when things are going poorly, we see many enterprises decline to invest in the future in favor of trying to resuscitate the Golden Goose. In this case they’re allocating to survival efforts over disruption.

In both cases, they’re failing to allocate adequate capital to disruption efforts. It’s a sort of “damned if you do, damned if you don’t” situation.

Process over product

One of my former Kellogg students announced to me with great excitement that she had been promoted to the role of VP of Innovation and Six Sigma. I tried—and unfortunately failed—to stifle a laugh. If that title isn’t oxymoronic, I don’t know what is.

Disruption requires purposefully coloring outside the box. Six Sigma is about defining a tight box, outside of which variances are undesirable unless it’s a continuous and controlled improvement.

Disruption blows up the local maximum in the hopes that an entirely new and better maximum can be found. Usually that means a significant decline in system performance in the near term. Such is the price of achieving what might be an order of magnitude improvement.

“The more you hardwire a company on total quality management, [the more] it is going to hurt breakthrough innovation. The mindset that is needed, the capabilities that are needed, the metrics that are needed, the whole culture that is needed for discontinuous innovation, are fundamentally different.”

– Vijay Govindarajan

I think the problem is more deeply rooted, however. It’s natural (and desirable) to establish process during the formation of a new product, team, or organization. Clearly understanding what you’re doing is a necessary precursor to measuring and improving it. The problem arises is when that procedural description transitions to a prescription.

If you ever hear the phrase, “that’s not how we do things,” you’ve probably run into a “process over product” problem. Continuous improvement has a natural tendency to turn descriptive processes into prescriptive ones. And prescriptive processes hamper experimentation and adaptability.

In the context of disruption, processes should be clearly defined but constantly tweaked, or even changed wholesale. That tends to be an alien concept for most enterprises, and where that’s the case it serves as a suffocating limitation on disruption.

Decision making

Decision making processes in enterprises are rarely optimized for disruption. Unfortunately, in our experience they’re often poorly optimized for execution, too. But even when that’s not the case, the effective decision making systems of enterprise leave much to be desired in the context of disruption. The most common problems we have identified include:

- Micromanagement and top down decision-making

- Decision by committee

- Requirement for sign-off: blocking rights, which are particularly bad when incentives are mis-aligned (e.g., IT)

- Tribal knowledge instead of data-driven decision

Hierarchical organizations typically fare poorly at disruption. Rapid disruption cycles, inherent coordination and communication costs, and the need for direct access to the voice of the customer mean that hierarchical decisions tend to be slow, poor, or (usually) both.

Decision by committee is an effective way to encourage consensus and bring to bear different viewpoints. In some organizations it’s required to coordinate disparate operating systems. But in the context of disruption, it almost always leads to slow and watered down decisions. Efforts to achieve consensus in groups leads to seeking the norm and avoiding frontier thinking. Of course, that’s precisely the opposite of what needs to happen for successful disruption.

Decision by committee, particularly large committees, also almost inevitably suppresses the diversity and volume of ideas by rewarding normalized conversation, leading to self-censorship of participants. It also serves to limit the contributions of any given participant, which tends to lead to an overemphasis on shared views to the exclusion of frontier thinking.

Requirements for sign-off rights operate similarly to decision by committee, but tend to have even more troublesome implications. When all it takes is for one person on a list to kill a concept, only a very narrow consensus path is typically left open. It also tends to result in politics and horse trading, which further waters down decisions.

Long-standing organizations have a strong tendency to devolve into tribal knowledge in place of data-driven decisions. Tribal knowledge can be very useful as a shortcut to avoid wasteful effort, but it’s generally preferably to rely on data to make decisions. In the context of disruption, tribal knowledge decisions are particularly challenging because tribal knowledge is much more likely to be erroneous in the context of a new domain or system.

Conclusion

We’re living in a world of ever faster change, and multiple forces and trends will likely accelerate the pace of disruption. Disruption is fundamentally different from execution, and as a result requires different approaches to organizational design and leadership. Unfortunately, most successful enterprises struggle mightily in the context of disruption for a combination of factors, most of which are rooted in the same things that made them successful in the first place.